Welcome as accounting with Bennet Tchaikovsky. Our topic today is the statement of cash flows. We're going to be going through a simplified example.2

This presentation is copyright 2008 to 2018 by Bennet Tchaikovsky all rights are reserved and if you have any questions please email me at 1812cpa@gmail.com or bennet1812@gmail.com.

So the example we're going to be going through today is for lasers ink and for lasers and we're going to be

Preparing a balance sheet. Excuse me. When be preparing a statement of cash flows.

For the year and December 31 2020 so if you have questions on how we go through and do this. I want to encourage you to go look at the other video that just may have been the basic cash flow questions. Okay.

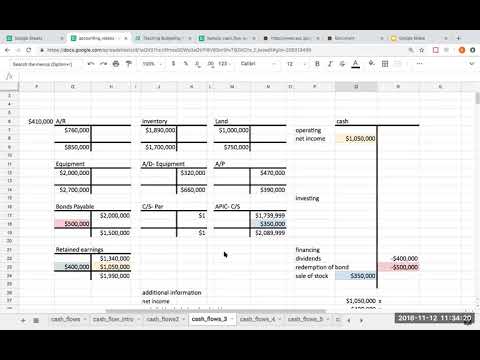

So the first thing when we look at a statement of cash flows is that I know what my answer is going to be my cash started out at 220,000

And it ended at 630,000 so my total increasing cash is going to be $410,000 so my first step when I go through and do these this question.

Is I want to prepare the skeleton for really, what is this cash flow going to be ultimately looking like. And when I prepare the skeleton. What I'm doing here is I'm gonna say the company name or lasers.

And statement of cash flow for the year ending

December 31 2020

And my cash and cash equivalents at the very beginning of the period were 220,000

This is

Might be getting cash was 220,000

My total cash increased by 410,000

And how did I get this is the difference between the 630,000

In cash minus 220,000 beginning

And so my ending cash balance is going to be my cash and cash equivalents at the beginning of the period plus this 410,000 or 630,000

Now the fun stuff begins here which is we're going to go through and now fill out the inner parts.

So our second step when we are doing a statement of cash flow when we're asked to prepare a statement of cash flows.

Is to go through and put all of this, these accounts into T accounts for the cash T account, we're going to go through and put in the various different categories operating, investing and financing.

So for your sanity and for mine. I'm going to pause this video while I go through and do that.

Okay, we're back. And what I've done here is I have taken this balance sheet and put it into T accounts.

Notice here accumulated depreciation on the equipment is a contra asset account. Therefore, it has a credit balance, please refer to my other videos in terms of how to go through and to do this and as a quick reminder

Sorry.

When I'm going through and recording transactions and which way they should fall on the balance sheet assets are debits

Liabilities and owner's equity generally have credit balances I increase assets with debits decreases with credits liabilities and owner's equity or increase with credits and decreased with debits so

Going back here to our example, the first thing I went through and did is I created a skeleton which is right here below.

The second thing I went through and did is I put in the opening opening and ending balances into each one of the t accounts for cash. What I'm more going to be doing here is I'm going to be breaking this down and operating

And investing

And financing.

In terms of what goes where I want to strongly suggest to you to go back and watch the earlier videos where I talk about what transactions go through into each one

So now that we've put the balance sheet into our T accounts here.

My next thing I'm going to be doing is I'm going to be dealing with the additional information. First I don't jump ahead and start analyzing the t accounts.

Until I have dealt with the additional information. First, the first one right here is it tells me that my net income was 1,000,050

When I go here and where does net income. Go. It goes to retained earnings. If you don't understand this. Please watch my previous video.

That is a simplified cash flow question that talks about what impacts retained earnings

So my net income was 1,000,050 net income increases retained earnings. And so what do I need to do well over here I'm need to put this on to into my cash T account.

So I've got 1,000,050 my rule is, I do the opposite the cash or unwilling to debit cash here for 1,000,050 and I'm going to call this net income because that's what it is.

So that's my first piece of additional information.

My next one here is cash dividends declared and paid for $400,000 what I'm paying a dividend. I'm going to go over here to retain earnings. Because remember, dividends decrease my retained earnings

I have a debit here for 400,000 and so when it comes to a dividend, where does it go well. Again, going back to the earlier discussions, when I'm paying a dividend.

This is kind of giving my owners a return on their investment for the most part. So what I'm going to do here is I'm going to do the opposite to cash.

But what section. Do I do it in because it relates to the company stock. I'm going to put it in the financing section. So here I'm going to show a credit to cash a 400,000 and my description is going to be dividends. So

That's what I'm doing here. Okay, so I'm dealing with the additional information I've dealt with this and I've dealt with this.

The next one that tells me here. Is it says that bonds payable of $500,000 were redeemed for $500,000 cash.

And let's take a look at this. So my bonds payable went from 2 million to 1.5 million. What is redemption mean it's not the Marley redemption song rather what it is, which was a great song. By the way,

Rather, what it is I'm buying back my bonds. So here I was more than likely crediting cash and then if I'm redeeming it I'm decreasing it. So I'm going to decrease that liability.

By this $500,000 so my bond payable here has a debit of 500,000 my rule is, I always do the opposite to cash. So what I'm going to be doing here is I'm going to be crediting cash for 500,000

And because I'm buying or selling my own bond, it goes in the financing section. And if you're having trouble with knowing what goes where generally everything related to a company's finances or their own securities is going to be

Is going to be in the financing section please refer to my other videos. If you're having troubles understanding that part. Okay.

So we've dealt with the bond redemption and again calling a redemption of bond because that's what it is. And then here I have common stock was issued for $350,000 cash. So my common stock when I'm issuing a stock. I'm going to be debating common stock and I'm going to be crediting

Additional painting capital. So here I'm going to do 350,000 excuse me, I'm going to be deafening cash crediting common stock par

crediting additional painting capital common stock. So here I have 350,000

What I'm dealing with my additional information I want to go through and kind of input in these transactions as though they had an impact on cash.

So here, common stock was issued for $350,000 cash. What does that mean, more than likely cash was debited additional paid in capital common stock and common stock at par were credited

So here I've got 350,000 showing as an increase to my additional painting capital common stock. What I'm then going to do is I'm going to do the opposite to cash or here have a debit to cash.

I'm going to call this a sale of stock or you could say, and issuance common stock issuance both those would be fine.

Okay, so I've dealt with the bond payable dealt with the common stock and now it's telling me that lamb. It costs 250 was sold for $200,000 cash.

So when I sell land or when I have any type of an asset sale. I'm going to have here, Miss case I'd be definite in cash credit and land for 250

If this was equipment, I would have an amortization question or a depreciation issue, but I don't. Because that's land. So if I sold land for that must mean, I'd be deafening cash for 250 and crediting land for 250,000

So where it is land go so I have to do essentially the opposite to cash. So where am I going to put this 250,000

When it comes to the purchase or the sale of property plant and equipment including land that is going to be showing up as an investing activity. So here, this is going to be a sale land.

And this is going to be the opposite of cash or a debit here of 250

And let's go ahead and do this here. So there we go. Okay, so I have now gone through and dealt with all of the additional information. The best way I can tell you to do. This is when you're getting here to the bonds redemption.

You know, and then the common stock, I would kind of think, well, what's happening to cash in this case here, I'm debiting cash and crediting common stock.

Here I'm repurchasing my own shares or my own bond. So I'm going to be crediting cash deafening bonds payable.

So let's now go up here and so now that we've dealt with the additional information. We're now ready to look at the various different accounts.

And again, my overall goal here is I need to get to an overall increase in my cash account of 410,000 so but the accounts receivable

Accounts receivable went from 760,000 to 850,000 or an increase of $90,000. So what do I do with this 90,000 well over here. I'm going to do the opposite to cash or credit of 90,000

Once I'm over here than I describe it. I say this is an increase in accounts receivable

My inventory went from 1,890,000 to 1.7 million what happened here. Well, in this case to balance my T account. I'm going to need a credit

Of 190,000 or 1,890,000 less 190,000 gives me 1.7 million. And so for this one right here. I'm going to do the opposite to cash or

Debit cash here for 190,000 when I go through and do this my description is going to match what happened in the t account. So this is going to be a decrease in inventory

And we'll make this just a little bit bigger for right now. There we go. Okay, so I have a decrease in inventory my land is already balanced. I've already addressed them.

Over here, my equipment went from 2 million to 2.7 million, what do I need to do to balance my T account. Well, I need a debit here.

Of 700,000

So what do I do to cash in this case here for my cash. What I'm gonna do is I'm going to do the opposite of cash and this here is going to be a credit to cash of 700,000

And what do I call this, I call this the purchase equipment.

In this here will be for 700,000 and whenever I'm buying or selling property plant and equipment. If I'm buying equipment for cash. It goes to the investing section if I'm selling equipment, the proceeds go into the investing section.

Okay, so I've got here accumulated depreciation on equipment. So here I've got 320,000 and I ended up at 660,000. So here I've got here, I need 340,000 to balance the t account.

And what I would normally do is, I would say, Okay, I'm going to follow the same role is over here.

I'm going to do the opposite to cash. Okay. And this is where students make a lot of mistakes and the mistake they make is, I'll say that. Oh, this is an increase in accumulated depreciation equipment. No, it's not. What causes this increase is going to be

The way I record depreciation expense is I'm going to debit depreciation expense for 340 I would be crediting accumulated depreciation here.

So when I'm using the description for accumulated depreciation on equipment. I'm going to be using the description of how it was generated

I'm going to follow the same rule for accumulated amortization or for the allowance for doubtful accounts, which would be amortization expense and bad debt expense respectively

So, respectively. Excuse me. So that's what I do here. Now remember again I don't call it an increase in accumulated depreciation on the equipment. I'm going to call it what it is, which is the depreciation expense.

For accounts payable. I went from 470 to 390 here to balance my T account. I need a debit of 80,000. What's my role I do the opposite to cash or I'm going to credit cash here for 80,000 and hopefully we can find another highlight color to use

Another we go little offline green. Perfect. Okay.

And so what is happening here with payables. Well, if I'm debiting accounts payable right remember because accounts payable typically has a credit balance if I'm debiting accounts payable.

This is going to be called a decrease in accounts payable right over here for 80000 so what I now do is I take a look at the rest of it accounts for bonds payable, I had an opening of 2 million credit here 500 and then we'll totally screwed this up.

This should just be 400,000 and that should be 500,000 I was jumping ahead. Okay, so here I have a credit for 500 I've dealt with this over here as a debit no change to common stock par

Additional paid in capital common stock credit to debit overhearing cash and then I have retained earnings. My which of my dividend here.

Shows up as a credit in the financing activity section. So my magic number is 410,000 so I add up all of these different balances it needs to equal to 410,000 so

Here in my operating section.

I'm 1,580,000 of debits 170,000 credits. So my total cash provided by operating

Is going to be 1,580,000

Minus 170,000 or 1,410,000

For investing activities, I had two things happening here.

And I have here 250,000 have a debit from my sale of land plus my purchase of equipment for 700,000 so this is going to be my total cash used in

Or 700,000 minus 250 or 450,000 remember if my credits outweigh my debits in the particular section. It's going to be used in not provided by so if the cash is a debit for the section. It's going to be provided by if it's, if it's a credit, it will be used in

Lastly here for financing.

I had here.

Debits have 350

Credits of 900,000 and kind of move these guys down here.

Over here.

Sorry additional information and to make a little more room. There we go.

So right over here. So my total cash here.

So my total cash.

Use in financing activities is going to be 550,000

When I add up the three amounts or cash provided by operating activities of a 1,410,000 my cash use in investing activities 450,000 and my cash views and financing activities of 550000 what I'm going to be ending up with here.

Is a total of what it should hopefully be my ending

cash balance.

Pricing, am I changing cash. I've got 1410 000

So my increasing cash.

Is going to be 410,000 okay

That was a lot. So let's go back here and kind of quickly review what we did. The first thing we had to go through and do is input in. So the first step is we made the skeleton.

Which is down here below. And we're going to get back to that in a second. But in the skeleton, we're just kind of inputting in the beginning cash balance, etc. The next thing I had to go through and do is I had to put in the beginning and balances into my T accounts.

Then I dealt with the additional information I put in the additional information into the t accounts.

Then after I deal with the additional information I go through and post everything into the cash account. Now remember, pretty much anything that's financing related if I'm paying a dividend. If I'm buying or selling a bond or if I'm buying or repurchasing shares goes into financing.

Anything, I'm doing with related to buying or selling equipment marketable securities or lamb those investing and then I've got everything else is pretty much thrown into operating

So once I put everything into the t accounts. I'm going to put give a total here for each area.

And that's what I just did right over here as I Total of each one total debits total credits if the amount was a total debit. It's going to be total cash provided by operating

If the total cash was a credit, it would be total cash used in investing. If it's over here if its credit. Again, it's going to be used in

So I added up those three areas that million for 10 which is coming from operating, investing, financing and my total change in cash was 410,000

You do not least on my exams. You do not need to show me this amount of detail. However, it's important that we're going through and doing this for this particular example. So let's take a look at what our statement of cash flows looks like and how we prepare it

Okay, now we're back. And this was the skeleton that I initially went for him prepared at the very beginning of the question. And note here from my skeleton.

All I did was I put in my beginning cash and cash equivalents. I put in my total change in cash and got to my ending amount

So right here, when I start going through and doing this. Now I'm going to flush this out so from my operating activities. I'm gonna have my net income by net income here was 1,000,050

And remember, if this amount on the cash is a debit. I show it here as a positive amount

So here from my adjustments need a little bit more space

A little bit.

OK.

So again, if I've taken the time to write my descriptions. They should be relatively easy to do.

Okay. And so here, my increase and accounts receivable is going to be 90,000 might decrease in inventory is going to be a positive 190 because it's a debit.

My depreciation expense is going to be 340,000 and why we are adding back the depreciation expense is because when we think about it.

Does depreciation have any impact on cash. The answer is no, because when we do this journal entry were essentially allocating the cost of a prior purchase.

So when it comes to handling the depreciation expense. This is going to be an add back to our net income because it has no impact on cash and then here I'm going to have a decrease in accounts payable.

Of negative 80,000

And here, my, my neck cash or my net cash provided by operating activities.

Is going to be

1,410,000 so

Now I get to my investing activities. I had here the sale of land I had here the purchase of equipment. So the sale of land is going to be a debit because it's positive. My sale of equipment will be a negative. So my net cash.

Use and investing activities.

It's going to be

450,000 notice I use total mission really be net

Okay.

And we'll do this one down here. I'm learning to everybody, we're all learning together. It's so much fun. OK. So now when I get to my financing activities. I think I'm gonna need a little bit more room here so we'll kind of scoop these guys up

Thank you, Google Sheets.

There we go. Google Sheets, great to use and classrooms. The students love them or are tortured by them. And so right over here. So my dividends, because it has a credit balance will be showing a negative amount

My bond redemption, because it's a credit will be shown as a negative and my sale of stock right here is going to be 350 so this is going to be my net cash used in financing activities.

And this is going to be a total of 550,000 when I add up the million for 10 plus the 450 plus the 550. That's what I get.

Lastly, I have no non cash transactions and we'll talk about that on the next one. And so there we go.

If you've done your T account here, this essentially is giving you the statement of cash flows. And so again, hope this video is helpful. And please remember to like and subscribe and I will see you in the next cash flow video, have a great one.

For more infomation >> Future of 81: Many at Rep. Katko's E. Syracuse town hall meeting prefer community grid option - Duration: 2:16.

For more infomation >> Future of 81: Many at Rep. Katko's E. Syracuse town hall meeting prefer community grid option - Duration: 2:16.

For more infomation >> 震撼! 陈玉林的背后有着强大的力量支持。 目标是推动吴秀波远离娱乐,他们是谁? 当真相曝光时,网友们大声喊道:我理解为什么吴秀波无法扭转这个案子! - Duration: 11:56.

For more infomation >> 震撼! 陈玉林的背后有着强大的力量支持。 目标是推动吴秀波远离娱乐,他们是谁? 当真相曝光时,网友们大声喊道:我理解为什么吴秀波无法扭转这个案子! - Duration: 11:56.  For more infomation >> Cần Bán Kawasaki z1000 Xanh Đen Giá Rẻ Liên Hệ 0787678774 - Duration: 1:01.

For more infomation >> Cần Bán Kawasaki z1000 Xanh Đen Giá Rẻ Liên Hệ 0787678774 - Duration: 1:01.  For more infomation >> DIY Slide Wire Canopy Kit

For more infomation >> DIY Slide Wire Canopy Kit

For more infomation >> Sarah Jakes Roberts - What I Called You To Do | The Potter's House At OneLA - Duration: 14:36.

For more infomation >> Sarah Jakes Roberts - What I Called You To Do | The Potter's House At OneLA - Duration: 14:36.  For more infomation >> Light Snow Along Grapevine - Duration: 1:25.

For more infomation >> Light Snow Along Grapevine - Duration: 1:25.

For more infomation >> Missouri Lawmaker Calls for Stricter Penalties on Fentanyl - Duration: 1:31.

For more infomation >> Missouri Lawmaker Calls for Stricter Penalties on Fentanyl - Duration: 1:31.  For more infomation >> Illini men's tennis falls to UNC - Duration: 0:30.

For more infomation >> Illini men's tennis falls to UNC - Duration: 0:30.  For more infomation >> Toyota Land Cruiser100 4.7i V8 Executive 7-persoons, Leder, Bijtellings vriendelijk, dak, 3.500 KG t - Duration: 1:08.

For more infomation >> Toyota Land Cruiser100 4.7i V8 Executive 7-persoons, Leder, Bijtellings vriendelijk, dak, 3.500 KG t - Duration: 1:08.  For more infomation >> Annual Hunt and Fish Outdoor Show Held - Duration: 1:21.

For more infomation >> Annual Hunt and Fish Outdoor Show Held - Duration: 1:21.

For more infomation >> Katalog Tupperware Februari 2019 - Duration: 5:41.

For more infomation >> Katalog Tupperware Februari 2019 - Duration: 5:41.

For more infomation >> [Việt Mix] Liên Khúc Nhạc Xuân / Happy New Year ft Vì Anh Thương Em Remix ► DJ Thành Đạt - Duration: 1:01:38.

For more infomation >> [Việt Mix] Liên Khúc Nhạc Xuân / Happy New Year ft Vì Anh Thương Em Remix ► DJ Thành Đạt - Duration: 1:01:38.

No comments:

Post a Comment